When you first bought your home, your credit score may not have been the highest. This is a situation many homeowners find themselves in. You agreed to a mortgage loan term, and as you became stronger within your financial situation, you believe you can obtain a lower interest rate. If you believe that you're paying an interest rate that's higher than what you should be paying, then your ideal solution may be to refinance your mortgage. Although this process can ultimately save you tens of thousands of dollars, if you're not careful, you could end up hurting your credit score according to your650score.com and ultimately paying more in fees and other miscellaneous costs. The following are the most common refinancing mistakes.

Mistake #1 – Not Understanding Your Credit Score

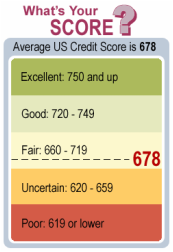

One of the biggest mistakes you can make within the process of refinancing your home is to not do your homework before agreeing to a refinancing term. The most important step to take before refinancing your mortgage is to fully understand your credit score and making sure there are no errors within its report. Your credit score is the foundation of your re-worked interest rate. Therefore, it's imperative to know whether or not your FICO score is high enough to secure a substantially lower interest rate (see here for more info).

You must also obtain a general idea of what your home is actually worth. While you can turn to several online sources for a basic-level understanding of your home value, the most effective way to determine your actual home value is to hire an official appraisal service. These services look at the quality of your home as well as the value of the surrounding property to provide an accurate home value. Walking into a refinance meeting with this information gives you the upper-hand when it comes to negotiating a lower interest rate.

Mistake #2 – Excessive Debt

While holding debt is key to fostering a high credit score, if your debit is out of control or if you have too many opened accounts, many mortgage lenders view you as high-risk. Therefore, before you even think about refinancing your home, you should take a close look at your open credit accounts and overall debt. One of the biggest mistakes is opening small lines of credit at various retail establishments, such as an electronics store. While you may think these are small debts, in the eyes of a mortgage lender, they are sources where your money must go. If you have too many of these small debts, you'll likely receive a not-so-desirable interest rate or be completely denied a refinanced home loan.

Mistake #3 – Not Shopping Around

Even if you are satisfied with your current lender, many homeowners rob themselves of thousands of dollars by not shopping around with different lenders. You should absolutely obtain quotes from various lenders. Don't assume your current lender will give you the best deal because you're a current customer. While you should obtain a quote from your current lender, use this quote as a way of negotiating better terms and lower interest rates with other lenders. Even if you decide to go with your current lender, you should never assume they are your ideal choice. Comparing refinanced interest rates with at least three lenders ensures you get the lowest interest rate possible on your home.

Mistake #1 – Not Understanding Your Credit Score

One of the biggest mistakes you can make within the process of refinancing your home is to not do your homework before agreeing to a refinancing term. The most important step to take before refinancing your mortgage is to fully understand your credit score and making sure there are no errors within its report. Your credit score is the foundation of your re-worked interest rate. Therefore, it's imperative to know whether or not your FICO score is high enough to secure a substantially lower interest rate (see here for more info).

You must also obtain a general idea of what your home is actually worth. While you can turn to several online sources for a basic-level understanding of your home value, the most effective way to determine your actual home value is to hire an official appraisal service. These services look at the quality of your home as well as the value of the surrounding property to provide an accurate home value. Walking into a refinance meeting with this information gives you the upper-hand when it comes to negotiating a lower interest rate.

Mistake #2 – Excessive Debt

While holding debt is key to fostering a high credit score, if your debit is out of control or if you have too many opened accounts, many mortgage lenders view you as high-risk. Therefore, before you even think about refinancing your home, you should take a close look at your open credit accounts and overall debt. One of the biggest mistakes is opening small lines of credit at various retail establishments, such as an electronics store. While you may think these are small debts, in the eyes of a mortgage lender, they are sources where your money must go. If you have too many of these small debts, you'll likely receive a not-so-desirable interest rate or be completely denied a refinanced home loan.

Mistake #3 – Not Shopping Around

Even if you are satisfied with your current lender, many homeowners rob themselves of thousands of dollars by not shopping around with different lenders. You should absolutely obtain quotes from various lenders. Don't assume your current lender will give you the best deal because you're a current customer. While you should obtain a quote from your current lender, use this quote as a way of negotiating better terms and lower interest rates with other lenders. Even if you decide to go with your current lender, you should never assume they are your ideal choice. Comparing refinanced interest rates with at least three lenders ensures you get the lowest interest rate possible on your home.

RSS Feed

RSS Feed